401(k) Investing Basics

401(k) Investing Basics

Reviewing Retirement Plan Investment Options and Information

It’s been three months since I started my new job and the retirement plan administrator just sent notice that it is time to sign up for my 401(k) plan.

In today’s post you will learn about a retirement plan’s basic workings and key terms you should know about.

This post is more for the new workers who are just starting their jobs and need to learn more about how their retirement plan works.

I know many of you already have retirement plans but this may be a good review and you may learn something new!

Benefits of Contributing to Your Retirement Plan

The main benefit of contributing to your retirement plan is you are saving for your future!

To live out a comfortable retirement you will need a nest egg so you can tap into to pay for living expenses.

Gone are the days of defined benefits plan (aka pension plans) where your employer pays a guaranteed retirement benefit to you.

And with talks about Social Security running out of money in less than ten years, your retirement savings (and hopefully cash flowing assets) will help pay for your living expenses in your golden years.

Another benefit of contributing to your retirement plan is the tax benefits.

For 2022, the yearly maximum contribution limit is $20,500. This means if you contribute the maximum to your retirement plan you can deduct this from your taxable income.

For example, if your income for the year is $75,000/year and you contribute $20,500 to your retirement plan, you will be taxed on only $54,500 of your income!

Another benefit of contributing to your retirement plan is tax free growth of the money invested. As long as the the money stays in your account and you don’t take any distributions, the money grows tax free. This helps your nest egg grow faster through compounding. Of course when you begin to withdraw from the account you will be taxed.

Oh you thought there was a free lunch?

The final benefit of contributing to your retirement plan is the “free” money you may get from your employer. This “free” money is the employer match.

Each employer is different but my employer will match 100% of the first 3% of my eligible compensation and then match 50% of the next 2% of my eligible compensation.

Your employer may be different but whatever they match it’s free money just for contributing to your future.

Retirement Plan Investment Choices

Each employer’s plan may be different so you have to check your specific plan to see what choices are available.

For my particular retirement plan, the default investment for me is a target date retirement fund by Vanguard.

Vanguard is a highly respected company in the investment space and is know for their low expense investment products.

A target date retirement fund sets an expected retirement year for you based on your expected retirement age and adjusts the portfolio into lower risk assets. The reason for this change is you don’t want your portfolio to significantly drop in value just as you begin retirement.

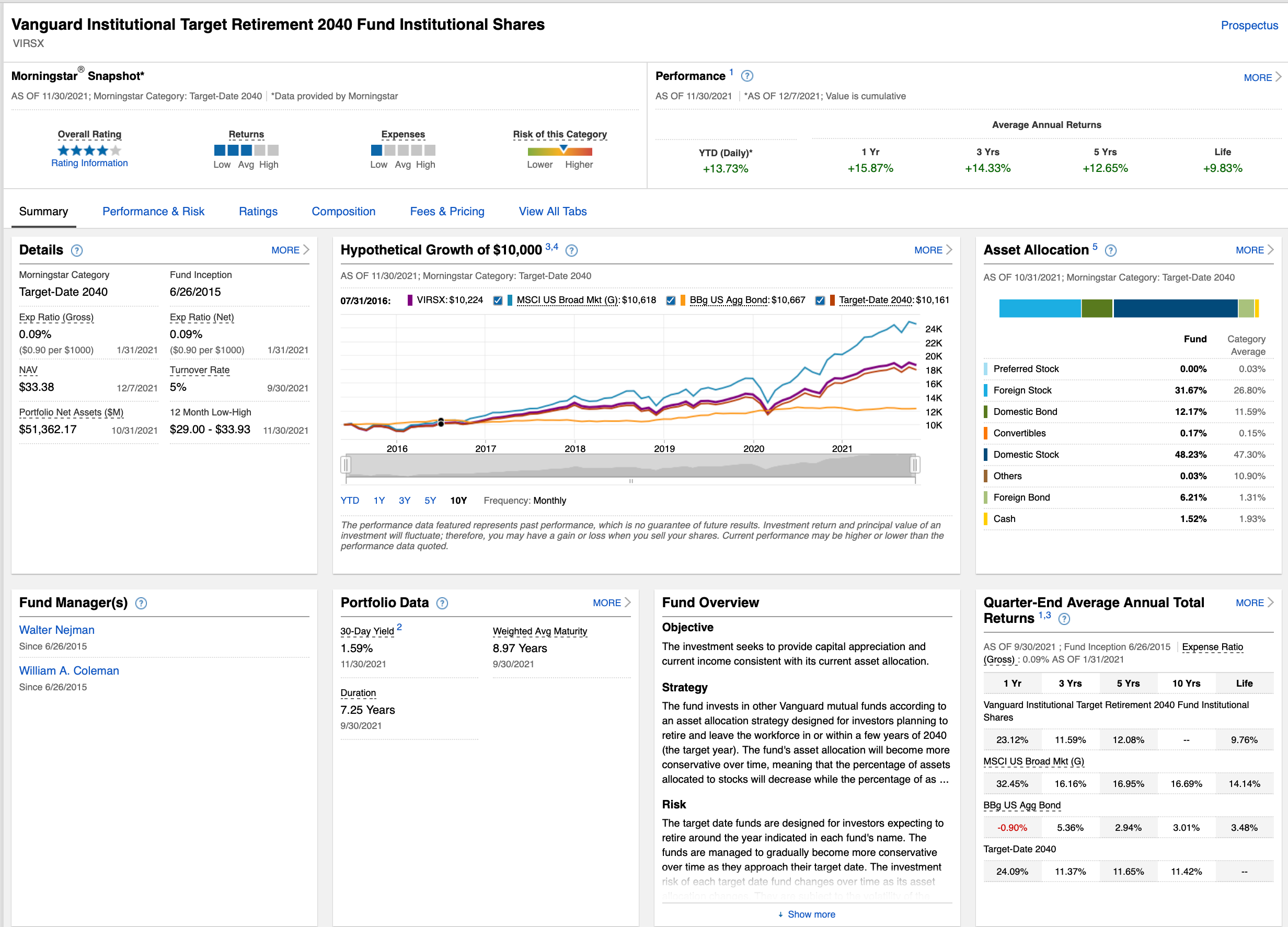

For my retirement plan, the default investment choice is Vanguard Institutional Target Retirement 2040 Fund (VIRSX).

I decided to keep this investment to keep things simple and the target date retirement fund was already going to be my first choice!

There are other investment funds for small/large cap stocks, bonds, income, and international equities I could have chosen but I decided not to invest in these funds because I don’t know much about them.

Key Retirement Plan Terms to Know

Learning about your retirement plan is like learning a different language.

But don’t worry!

Below I have listed key terms you will need to know about your retirement plan.

Prospectus

The prospectus has all the “fine print” about the fund. It contains the annual report, semi-annual report, portfolio holdings, investment strategy, etc. It’s a good idea to read this as it gives you a lot of information about what you are actually investing in.

Rollover

A rollover is the transfer of funds from one retirement account to another.

If you are leaving your employer it is a good idea to transfer the retirement into one consolidated account.

If you perform a rollover there is a time limit on when you must deposit the funds into the new account.

If you don’t, the transfer will count as a distribution and you will be taxed and penalized for it.

Expense Ratio

This is the % of your assets under management that is paid to the fund’s administrators.

The fund managers are responsible for taking care of the fund and selection of the fund’s assets.

For VIRSX, the expense ratio is 0.09%!

This means that for every $1,000 I have invested it costs me just $0.90. This is VERY reasonable to have professionals take care of the fund.

All you do is buy shares!

Compare this expense ratio to my very first retirement plan where they charged 1.75% after taking their commission of 5% off the top!

Portfolio

The portfolio is what is specifically inside all of your investments.

It is the individual stocks or bonds that makes up the total of your investments.

Every portfolio is different but for VIRSX, the top four holdings are Vanguard Total Stock Market Indx I, Vanguard Total International Index Inv, Vanguard Bond Market II Idx Inv, and Vanguard Total Intl Bd II Idx Admiral.

Asset Allocation

Asset allocation is the types or groups of investments in the fund.

For example, in VIRSX the fund’s assets are spread across preferred stock, foreign stock, domestic stock, foreign bond, domestic bond, and cash.

The VIRSX fund is also diversified across countries and regions.

Consistency and Discipline Will Be Key

With retirement on the horizon I know that consistently contributing each year will be key. Retirement (?) is just 20 short years away for me and for many of you as well. You get to contribute EACH year but if you miss a year of adding to your nest egg you don’t get it back.

If you are young and just starting your career, 20 years will pass by quickly.

Make savings a habit and your future self will thank you for it.